The global economy was dealt a devastating blow by the coronavirus, and as it struggled to recover, geopolitical tensions such as the Russia-Ukraine conflict further hindered progress in 2022. Before a resolution could be reached, the Israel-Gaza conflict further exacerbated the situation, leading to increased geopolitical fragmentation.

These disturbances and fragmentations had a significant impact on international commodity prices, causing them to soar. The already high production costs in 2022 were further exacerbated by the skyrocketing prices of international commodities, leading to a scarcity of products and higher import costs for countries heavily reliant on raw materials.

This challenging situation placed immense pressure on governments and central banks worldwide, as they witnessed inflation rates reaching unprecedented levels. India, however, stood out in its successful management of this crisis. The proactive measures implemented by the Government of India and the Reserve Bank of India played a crucial role in curbing the inflation trajectory while maintaining a high growth rate.

India’s Triumph Over Inflation and Sustained Growth

In April 2022, India experienced a peak in CPI inflation at 7.8%, largely driven by surging crude oil prices and other international commodity prices. While CPI inflation showed signs of easing, it remained above the RBI’s upper band for an extended period. However, in recent months, CPI inflation has demonstrated significant improvement, falling to 5% in February 2024, 4.85% in March 2024, and further decreasing to 4.83% in April 2024.

The Wholesale Price Index (WPI) inflation, which reached a concerning 16.6% in May 2022, gradually decreased to 10.7% in September 2022 and continued its downward trend, reaching 1.3% in March 2023. By October 2023, WPI inflation had decelerated to -0.5%, with minor fluctuations in the following months: 0.2% in February 2024, 0.5% in March 2024, and 1.2% in April 2024.

India’s Inflation Trends (WPI and CPI)

Source: Reserve Bank of India

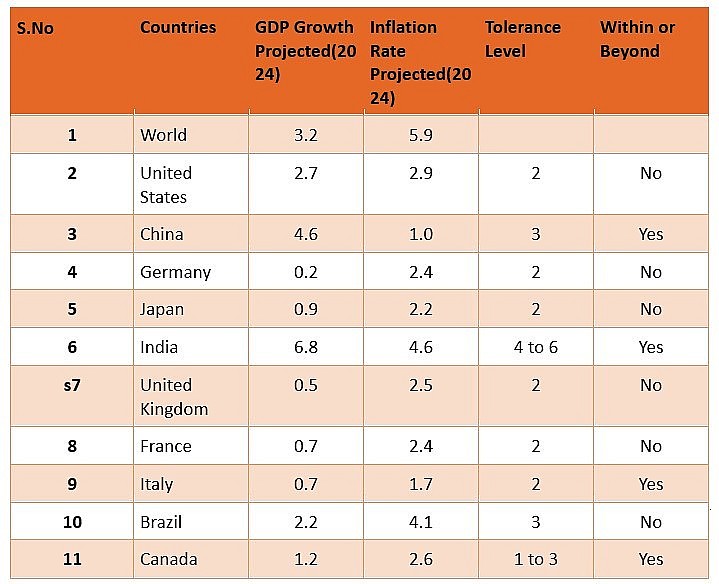

India’s remarkable achievement lies in successfully softening the inflation trajectory while maintaining consistent high growth. With an inflation rate of 4.8%, India remains within the RBI’s target band of 4-6%, and its GDP growth is outpacing that of the other top ten economies. According to projections, India will lead the way with a growth rate of 6.8% in 2024, followed by China at 4.6% and the US at 2.7%. Additionally, the IMF estimates India’s inflation rate for 2024 to be 4.6%.

Among the top ten economies, China is expected to maintain its inflation rate at 1%, well within its 3% tolerance band. Canada’s inflation rate of 2.6% is projected to remain within its 1-3% tolerance band, while the US inflation rate of 2.9% is forecast to exceed its 2% tolerance level. India’s robust economic performance highlights its resilience and potential to sustain rapid growth while effectively managing inflation.

A Comparison of GDP Growth and Inflation Rates Among the Top 10 Economies

|

| Source: WEO April 2024, IMF. Yes indicates that inflation is within the tolerance level; No indicates that inflation has exceeded the tolerance level. |

In recent months, CPI inflation in India has witnessed a significant decline, thanks to a continuous decrease in housing inflation (from 3.2% in January 2024 to 2.6% in April 2024), fuel and light costs (-0.6% to -4.2% during the same period), clothing and footwear (3.3% to 2.8%), and pan, tobacco, and intoxicants (3.2% to 2.9%). However, food and beverage inflation remains relatively high at 7.8% in April 2024.

The Indian government’s proactive measures to strengthen supply chains are contributing to the softening of inflation across various items. Looking ahead, India’s inflation trajectory is expected to normalize by September/October 2024, as the country’s kharif crops enter the food grain markets, boosting existing supplies. The conscious efforts to tame inflation and the solid fiscal consolidation path will further enhance India’s appeal to global investors.

{kind=link}